U.S. blocks Nippon Steel / U.S. Steel · Dec 2024

You can’t forecast a shock like this. But you can carry an expectation into it. The PRR Framework reads how each firm’s value has moved across the regulatory event class — every other event of this kind. Leave this event out, and the class still tells you which firms are wired to gain and which to lose. That’s the read you’d have walked in with.†

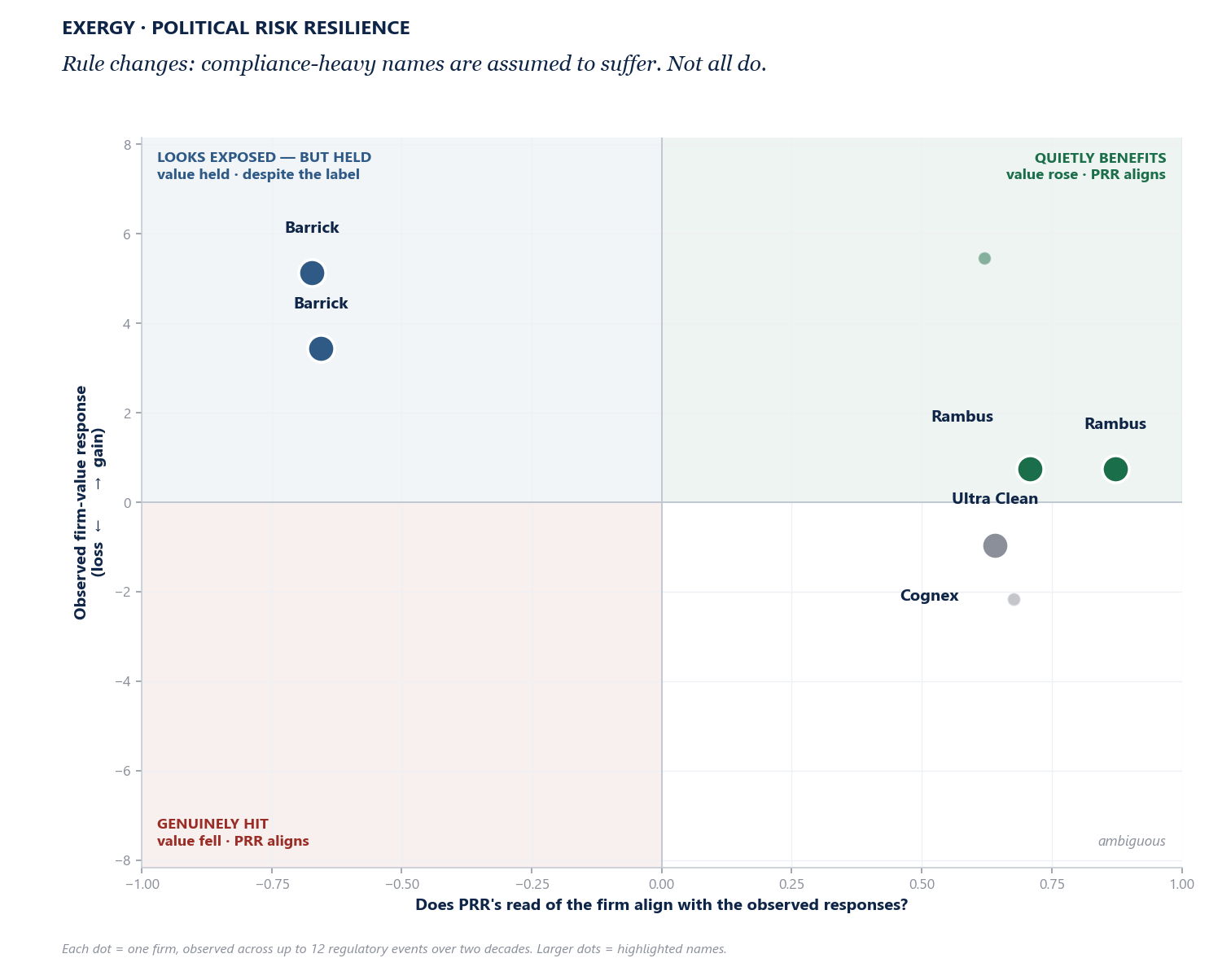

Before the event · what the class led you to expect, and what happened

The event lifted most of the basket — 7 of 8 names rose, led by the firms PRR’s class flagged as wired-to-gain: Am. Superconductor · Rambus · Rambus.

Why it matters — the next shock

That is the information gain. PRR can’t tell you when the next regulatory shock lands or how hard. It can tell you what to expect: the firms the rule change favors tend to hold or gain, while the names most exposed take the hit. You carry that read into the next one.

The full class behind the read

This event is one observation. The expectation rests on the whole regulatory class — the structure the single event is drawn from.

| Firm | Class expectation (ex-event) | On the day | Class alignment |

|---|---|---|---|

| Rambus | +0.4% | +25.8% | strong (ρ +0.87) |

| Rambus | +0.4% | +25.8% | strong (ρ +0.71) |

| Barrick | +5.1% | +10.0% | strong (ρ -0.67) |

| Cognex | -1.0% | +5.2% | strong (ρ +0.64) |

| Ultra Clean | -1.0% | +5.1% | strong (ρ +0.64) |

| Barrick | +3.5% | -0.5% | strong (ρ -0.66) |

† Method (beta, stylized example). A recognizable event chosen to illustrate the edge — not a comprehensive backtest. “Class expectation” = the firm’s mean value response across all other regulatory events (the focal event left out), 30-day window. “On the day” = the firm’s 30-day market-adjusted (abnormal) return around the event. “Class alignment” (ρ) = whether PRR’s firm read corresponds to which events moved the firm most. Firm value via cumulative abnormal return (CAR) in beta; more metrics planned. Exploratory / candidate-stage — association, not causation. PRR tells you what to expect; it does not forecast.